Budgeting Without Misery

Most budgets are built to punish every purchase. Here's how to design one that can actually absorb real life.

You've tried the spreadsheet. You've tried the app that pings you every time you buy coffee. You've felt the specific shame of overspending your "dining out" category by eleven dollars and quietly abandoning the whole system by the second week.

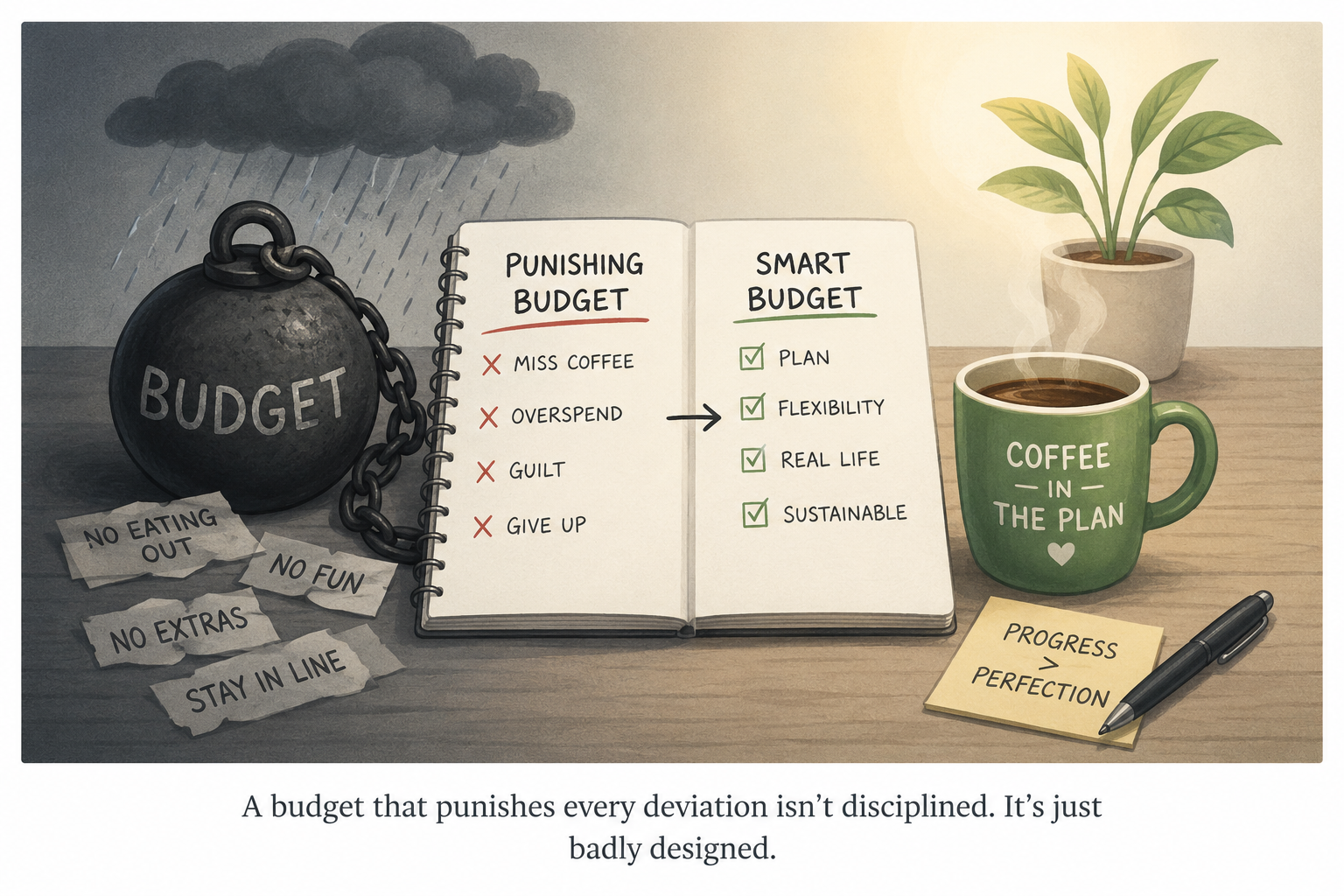

Here's what nobody tells you: that's not a willpower failure. Budgeting without misery is possible, but not with the kind of budget most people are handed, one built to flag every single deviation as a failure. A system that punishes normal human variance isn't strict. It's fragile, and fragile systems get abandoned.

The fix isn't more discipline. It's a different design, one that tells the difference between a real problem and ordinary noise. Here's how to build it.

Why Budgeting Feels Miserable (It's Not You, It's the Design)

ROOT CAUSE: The system is optimized for the wrong outputMost personal budgets are quietly optimized for one thing: zero deviation. Every category has a hard ceiling. Every dollar over that ceiling is treated as a failure, regardless of whether it actually threatens your financial stability.

That's the wrong output to optimize for. The actual goal of a budget isn't perfect adherence. It's sustainable financial stability, hitting your savings target, staying out of high-interest debt, building toward your goals, while still being able to live an actual life. A budget optimized for zero deviation instead of that real outcome will "succeed" for about three weeks and then get abandoned, because no system survives being treated as a pass/fail test every single day.

A budget that can't tolerate a normal week isn't a system. It's a countdown to quitting.

The fix is understanding what your budget is actually reacting to, and building in room for it on purpose.

The Mechanism: Why Every Budget Needs Room for Life Noise

In engineering, variance is the normal, expected fluctuation a system experiences that isn't a sign of failure, it's just how real systems behave. Life Noise is the same idea applied to your money: a slightly higher grocery bill one week, a friend's birthday dinner, a car that needed gas twice. None of it means your system is broken. It means your system is being used by an actual human being.

A budget that treats every instance of Life Noise as an emergency will always feel miserable, because it's asking you to react to something that was never actually a threat. The fix engineers use for exactly this problem is a deadband, what we call the Steady Zone: an intentional range where the system holds steady without overreacting to noise. Your budget needs one too.

The takeaway isn't "budget less carefully." It's the opposite: design the tolerance range on purpose, instead of discovering it by accident every time you blow past a category and quit for the month.

How to Build a Budget That Can Actually Absorb Real Life

Four steps, and none of them require a stricter spreadsheet.

1. Diagnose the Real Output

Write down what your budget is actually for: a savings number, a debt payoff date, staying out of your overdraft. Not "spending less" in general. A vague output can't be measured, and can't be protected.

2. Design Your Steady Zone

For your two or three highest-friction categories, set a range instead of a hard ceiling: not "$400 on groceries" but "$380 to $430." Anything inside that range is Life Noise. Nothing to react to.

3. Implement the Real Trigger

Decide, in advance, what actually counts as a problem: three months in a row above the range, or a single month that also threatens your savings transfer. That's your real threshold, not every individual dollar.

4. Iterate Monthly, Not Daily

Review the trend once a month, not the balance every day. A system you check obsessively will always find something to panic about. A system you review on a schedule tells you what actually matters.

Set One Steady Zone

Pick the one budget category that causes you the most guilt right now, groceries, dining out, or shopping.

You've just turned one rigid rule into a real system, the kind that can survive an actual month of actual life.