Money Systems:

Managing Resources and Risk

Your financial stress is not a math problem. It is a design problem. Here is the complete architecture of a money system that builds wealth, absorbs shocks, and runs without constant intervention.

You make a reasonable income. You are not reckless with money. You do not spend extravagantly. Yet, at the end of most months, the number in your account is lower than you expected it to be and you are not entirely sure why. You have a rough sense of your spending. You know you should be saving more. You handle financial surprises by hoping they are not too expensive.

The problem is not that you lack financial knowledge. You know what a budget is. You know compound interest matters. You know you should have an emergency fund. The problem is that knowing these things has not produced a system that acts on them reliably, without requiring constant attention and willpower to operate.

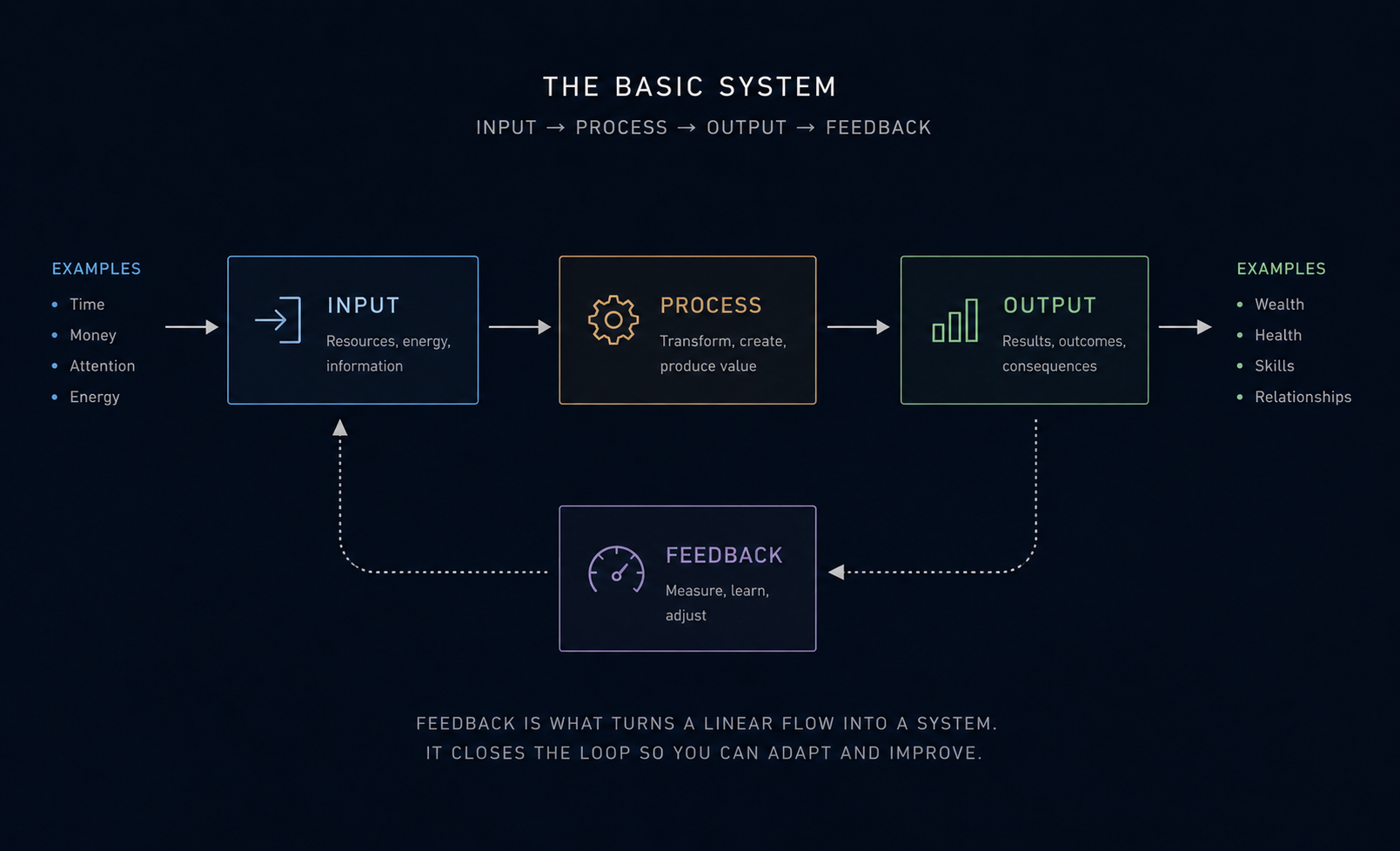

A money system is not a budget. A budget is a plan. A money system is a structure. One that takes income as an input, runs it through defined processes, produces specific outputs (savings rate, debt trajectory, net worth), and has feedback mechanisms that tell you whether it is working. Most adults have the input. They are missing everything else. This article builds the rest.

The Diagnosis: Why Most Money Systems Are Undesigned

ROOT CAUSE: No system was ever builtThe most validated financial literacy research in the world asks three questions. They cover compound interest, inflation, and risk diversification. These are the three foundational mechanisms of personal financial management. Together, they are known as the "Big Three." The findings, replicated across fifteen countries and multiple decades, are consistent: the majority of adults cannot answer all three correctly.

Sources: Lusardi (2020) PMC7393029 · Lusardi & Mitchell (2021) PMC10060204 · TIAA-GFLEC P-Fin Index

These are not statistics about laziness or irresponsibility. They are statistics about a knowledge gap that was never closed, and a system gap that followed directly from it. You cannot build a money system you do not understand. You cannot manage a feedback loop you have never been shown. You cannot maintain a resilience buffer when nobody taught you what adequate resilience looks like or how to measure it.

The goal of a money system is not to spend less. It is to produce a specific output (wealth, resilience, optionality) reliably, from the income you already have.

The Money System: Anatomy and Failure Modes

Before you can fix a money system, you need to be able to see it as a system. That means identifying its components — not conceptually, but specifically in your own financial life.

The System Anatomy

Business · Benefits

Debt service · Investment

Resilience Wealth trajectory

Shock absorption

Figure: Money System anatomy. Most people have the input. The process is undesigned. The feedback loop is absent.

Three observations about this diagram that matter for diagnosis. First: income is only one variable in the system. The output is determined entirely by this process: how decisions are made about allocation, savings rate, debt management, and investment. Second: the output is not how much you spend or save this month. It is the trajectory of net worth and resilience over time; a stock, not a flow. Third: without the feedback loop, the system produces whatever it produces, invisibly, until the output is bad enough to force attention.

The Big Three: What the System Requires You to Understand

The Lusardi-Mitchell "Big Three" financial literacy questions are not trivia. They identify the minimum conceptual knowledge required to operate a money system competently. You do not need a finance degree. You need to understand these three mechanisms and be able to apply them to your own situation.

The Five Failure Modes — Money Systems

Every money system failure maps to one of the five DB root cause types. Identifying which type is operating in your system points directly to the category of fix required. Different root causes require different corrective actions.

Building Your Money System: The Four Layers

A functional money system is not a budget. A budget is a monthly spending plan. A money system is the architecture that determines how every dollar that enters your life is allocated, measured, and grown. It has four structural layers, each with a defined purpose and a specific output to measure. You build them in sequence and each layer enables the one above it.

Layer 1 — Commitments Architecture

Before you can manage cash flow, you need a complete picture of your fixed monthly obligations and every recurring expense that exists regardless of what you do this month. Rent or mortgage, debt service, subscriptions, insurance premiums, utilities. Add them up. Divide by your monthly take-home income. That ratio is your commitment load. If it exceeds 60%, your system has no slack. In other words every variable expense competes for the remaining 40%, and any income disruption immediately threatens the fixed layer.

The diagnostic question: is your commitment load a deliberate architectural decision, or did it accumulate incrementally without anyone ever reviewing it in aggregate? For most people, it is the latter. Mapping it explicitly, often for the first time, is the starting point for every other layer.

Layer 2 — Cash Flow Allocation

Cash flow allocation is the process layer: how income moves from arrival to destination. A designed allocation process defines, in advance, what happens to every dollar before it arrives. Fixed commitments are covered automatically. A defined percentage flows to savings before any discretionary spending occurs. Variable spending operates within the remaining allocation, not against whatever happens to be left.

The critical design principle: savings is not what remains after spending. It is the first allocation, made before spending decisions begin. Reversing this sequence, saving whatever is left at the end of the month, is the single most common structural failure in personal money systems and the most reliably correctable.

Layer 3 — Resilience Buffer

The resilience layer is the shock absorber that makes everything else survivable. Its function is not to grow wealth. It is to prevent a single adverse event from cascading through every other domain. Three to six months of essential living expenses, held in a liquid account that earns at or above inflation, is the design specification.

Essential living expenses are not your current monthly spending. They are the minimum required to maintain housing, food, transportation, and essential insurance if income stopped today. That number is almost always lower than people expect, which means the buffer target is more achievable than it appears. The barrier is not math. It is that nobody ever told them the target or the sequencing: resilience before investment, always.

Layer 4 — Wealth Architecture

The wealth layer is where compound interest operates on your behalf, but only after Layers 1 through 3 are functional. Investment decisions made before the resilience buffer is funded produce a system with no shock absorption: investments must be liquidated at unpredictable moments, often at losses, to cover expenses the buffer would have handled. The sequencing is not optional. It is the engineering specification.

Within the wealth layer, the design principle is simplicity before sophistication. A three-fund index portfolio covers the entire diversification requirement of the Big Three framework. Complexity in investment management tends to produce higher costs, not higher returns. The system should be robust, not clever.

Running the System: Three Metrics, Two Cadences

A money system without measurement is a money plan, and plans expire. The feedback loop is not optional. It is the mechanism that turns a static design into a self-correcting system. Here are the three metrics that matter and the cadence at which to review them.

Monthly — Cash Flow Review (30 minutes)

Actual income versus planned allocation. Variable spending by category versus budget. Savings rate achieved versus target. This review does not require a complex spreadsheet. It requires honest comparison of what actually happened against what the system was designed to produce. Deviations are not failures, instead they are diagnostic signals. Each one asks: is this a one-time variance or a systematic gap requiring a design change?

Quarterly — Net Worth Update (60 minutes)

Total assets minus total liabilities, calculated consistently, four times per year. This is the output metric for the entire money system. It is the number that reflects whether the design is actually producing the intended result. Most people have never calculated their net worth. Calculating it quarterly transforms it from an abstraction into an instrument.

Annually — System Architecture Review (half day)

Once per year: is the commitment architecture still appropriate for your current income and life stage? Has the resilience target been met? Is the savings rate producing the net worth trajectory you specified as the target output? Annual reviews are where the system is redesigned, not just measured. Life stages change and the money system must change with them, deliberately and on schedule.

Map Your Current Money System

Open a blank document. This is not a budget. It is a diagnostic map of the money system you are currently running. It is the design that exists right now, regardless of whether you designed it. Write down your actual numbers for each of the four layers:

LAYER 2 — CASH FLOW: What percentage of your income goes to savings before discretionary spending begins? (If the answer is zero or "whatever is left," write that down explicitly.)

LAYER 3 — RESILIENCE: How many months of essential living expenses do you currently have in liquid savings? What is the target? What is the gap?

LAYER 4 — WEALTH: What is your current net worth? Assets minus liabilities. (Use estimates if exact numbers are unavailable. Write a number, not "I don't know.")

RCCA: Which of the five failure modes best describes the biggest gap in your current system?

You now have a financial system map. It is the most useful financial document you own, because it shows the architecture and not just the balance. The next action in this series builds the corrective action from what you just found.