Understanding Cash Flow

Your budget can look perfectly fine on paper and your account can still hit zero on the 27th. Here's why, and what to build instead.

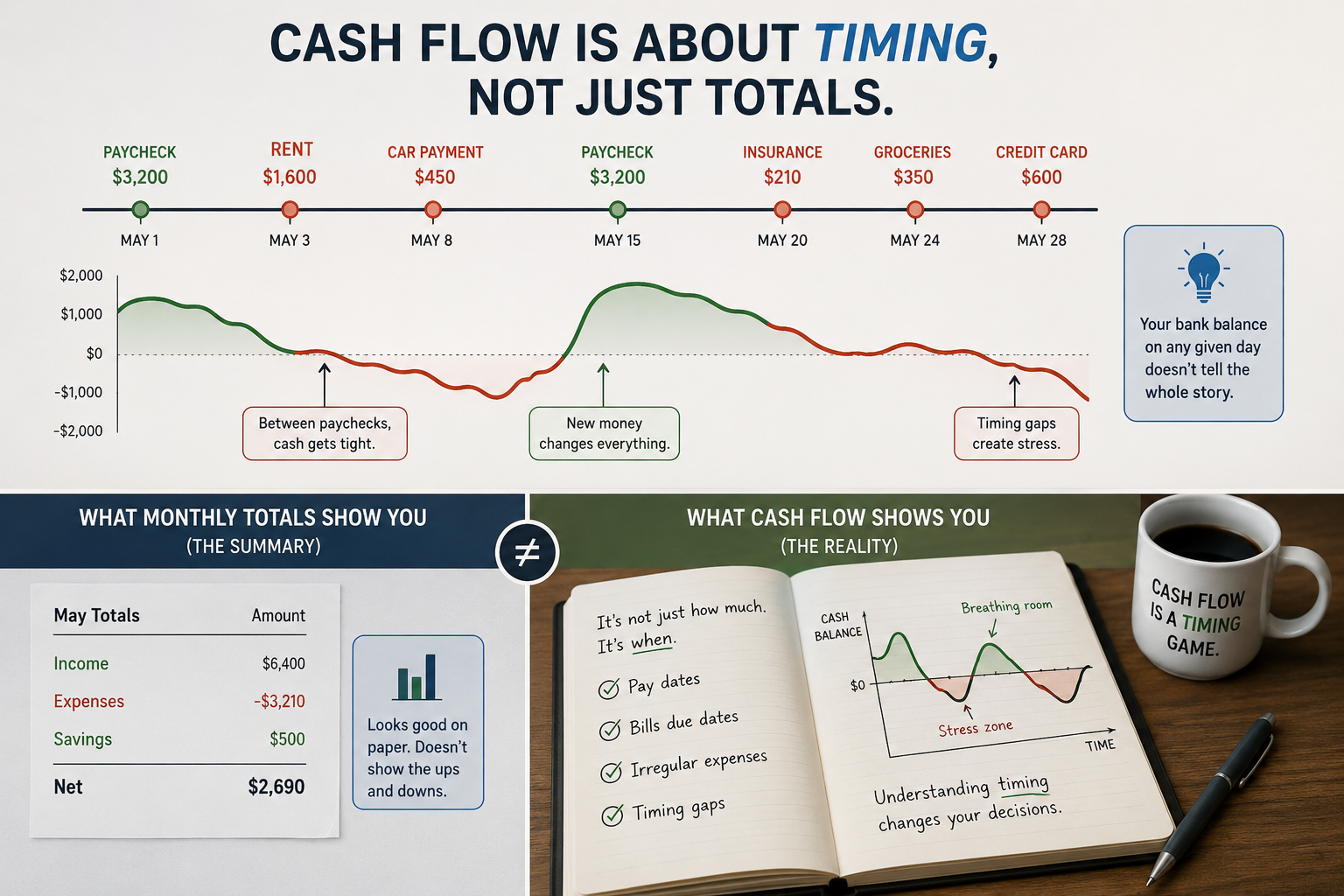

You did the math. Income minus expenses. The number is positive. You should be fine. And yet, three days before payday, your account is somehow at eleven dollars, and you have no idea how that happened.

This is the single most common financial confusion people bring to Deadband Life, and it isn't a budgeting problem. Understanding cash flow means understanding something your monthly totals will never show you: the timing of when money actually moves, not just how much of it exists on paper.

A healthy total and a healthy cash flow are two different systems. You can have both, one, or neither. Here's how to tell the difference, and how to build a system for the one your budget isn't already tracking.

Why Understanding Cash Flow Feels Impossible (It's Not You, It's Missing Feedback)

ROOT CAUSE: The system has no feedback loopMost people's financial "system" is really just a monthly total: income in, expenses out, net positive or negative. That total is real information, but it measures the wrong thing. It tells you the destination without telling you the route, and cash flow problems live entirely in the route.

Rent hits on the 1st. Your paycheck lands on the 15th and the 30th. A big expense lands on the 3rd, right after rent, right before any income has arrived to cover it. Every one of those events is individually normal. Stacked together, with no system tracking the order they happen in, they produce a cash crunch that a monthly total would never predict.

Your monthly total tells you if you're winning. Your cash flow tells you if you're about to run out of runway on a Tuesday.

Without a feedback loop tracking timing, you only find out about a cash flow gap the same way most people do: an overdraft fee, a declined card, or a stomach-drop moment checking your balance. That's reactive management, and it's fixable.

The Mechanism: How a Healthy Total Still Redlines

In engineering, an overloaded system is pushed past its capacity in a specific moment, even if its average load is perfectly fine. Redlining is that same event applied to your money: the specific day your outflows exceed what's actually landed in your account yet, regardless of what your monthly total says. A system can redline dozens of times a year while still looking "balanced" on paper.

This is exactly why cash flow understanding and budgeting are related but distinct disciplines. A budget manages categories and totals. Cash flow management manages sequence: which dollars arrive, in what order, relative to which obligations leave.

None of this means your budget is wrong. It means it's answering a different question than the one that actually causes financial panic. Cash flow is the missing layer underneath it.

How to Build a Simple Cash Flow Tracking System

You don't need forecasting software. You need one calendar and four steps.

1. Diagnose the Timing

List every recurring inflow and outflow with its actual date, not its month. Paycheck on the 15th and 30th. Rent on the 1st. That's it, that's the whole first step, and most people have never written it down this way.

2. Design the Danger Zones

Look for any date where a major outflow lands before the inflow that's supposed to cover it. That gap is your redline risk, the specific day cash flow problems actually happen.

3. Implement a Timing Buffer

For each danger zone you find, hold a small cushion in your account specifically to bridge that gap, separate from your general savings. This is a narrower, more targeted version of the contingency buffer covered in Article #57.

4. Iterate Each Time Your Schedule Changes

A new job, a new rent due date, or a new subscription resets your timing map. Review it any time a recurring date changes, not on a fixed calendar, since that's when a working system quietly breaks.

Map Your Timing Gaps

Open a blank document. List your next 30 days of expected income and your five largest recurring bills, each with its actual date.

That's your first real cash flow map, and it will explain more about your last six months of money stress than any monthly total ever could.