Emergency Systems:

Preparing for the Unexpected

An emergency doesn't disrupt one part of your life — it cascades into all of them simultaneously. The only variable is whether your systems were designed to absorb the shock, or to collapse under it.

You have thought about this. Not often, I would wager because thinking about it is uncomfortable, so you do not dwell. But somewhere in the background of your daily life is the knowledge that a single bad event could unravel most of what you have built. A job loss. A medical emergency. A major home failure. A car that cannot be repaired. You know the vulnerability is there. You have not built the system to address it, because building it means acknowledging it fully, and that feels like inviting the problem in.

The irony is that avoiding the design does not reduce the risk. It only ensures that when the disruption arrives, and for most adults, some version of it will, you face it without the architecture that would have made it survivable rather than catastrophic.

This article is not about worst-case scenarios. It is about the engineering principle that makes any system resilient: design for the foreseeable failure modes before they arrive. In engineering, this is not pessimism. It is the standard practice that separates systems that survive disturbance from systems that fail under it.

The Diagnosis: Why Most Households Have No Resilience System

ROOT CAUSE: No resilience layer: the system cannot tolerate disturbanceThe most rigorously validated household emergency preparedness instrument in existence, the Household Emergency Preparedness Instrument (HEPI) which was developed through a Delphi process involving 154 international experts across 36 countries, measures preparedness across multiple dimensions simultaneously. Its consistent finding is that preparedness gaps do not occur in isolation. Adults who lack a financial resilience buffer also tend to lack documented plans, organized insurance information, and established communication protocols. The gaps cluster because they share the same root cause: the resilience system was never designed as a system.

Sources: FEMA Community Resilience Indicator Analysis 2022 · Murphy et al. HEPI (2021) · Argonne / FEMA 2023

These gaps are not the result of indifference. They are the result of a system that was never built, and never built because nobody framed it as a system that needed building. Emergency preparedness is typically presented as a checklist: get a kit, make a plan, stay informed. That framing treats it as a set of discrete tasks rather than an integrated resilience architecture with interdependent components. Checklists expire. Systems persist.

Resilience is not what you have when things go wrong. It is what you built before things went wrong. The only variable is timing.

Why Emergency Systems Are Severity Tier 1: Cascade Risk

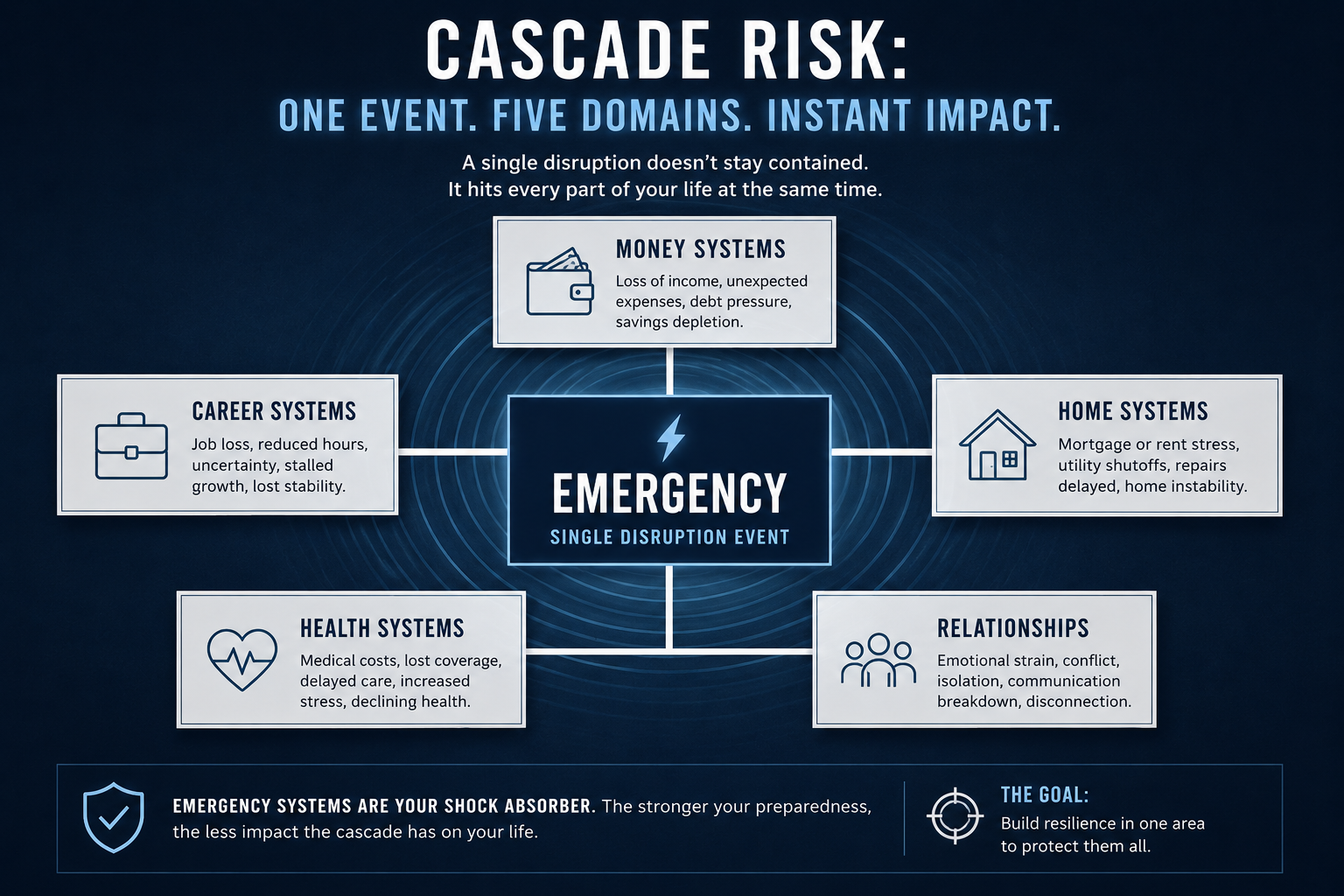

Every domain in the Life Systems Stack is important. Emergency Systems is classified Severity Tier 1 for a specific structural reason: it is the primary domain where a single failure event simultaneously disrupts multiple other life systems at once. This is what cascade risk means, and it is not hyperbole, it is the observable pattern of how emergencies actually propagate through a household.

A job loss is simultaneously a financial event (income stops), a career event (trajectory is disrupted), a health event (insurance coverage is threatened), a housing event (mortgage or rent payments are at risk), and a relationship event (financial stress is one of the most documented sources of relationship strain). An uninsured medical emergency is simultaneously a financial event, a health event, a career event, and a potential housing event. The cascade is not speculative. Actually, it is the documented pattern of how unprepared households experience acute disruption.

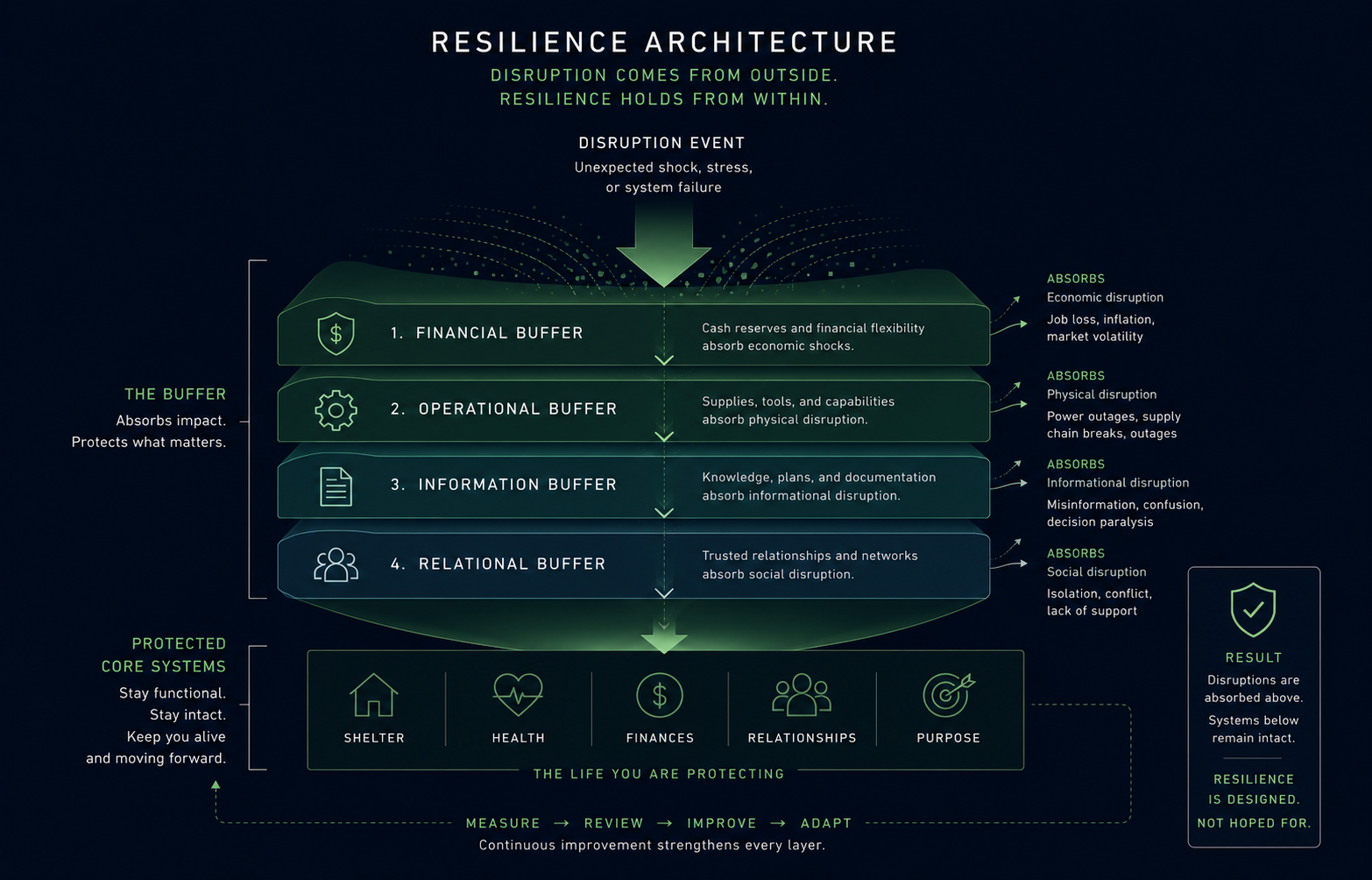

The Emergency System Anatomy

With the cascade mechanism understood, the system anatomy becomes clear. The Emergency System has four input categories, a planning and decision process layer, and a single critical output: absorption capacity or the ability to sustain a disruption without triggering a cascade into other domains.

Supplies + equipment

Documents + insurance

Skills + network

Evacuation routes

Decision triggers

Recovery sequence

Capacity Disruption contained

No cascade triggered

Figure: Emergency System anatomy. Most households have partial inputs. The process layer — plans and protocols — is almost universally absent.

The Six Dimensions of Household Preparedness

The HEPI instrument's dimensional structure provides the most rigorously validated framework for what household emergency preparedness actually requires. These six dimensions are not a checklist. They are the six functional areas that the system must address to produce genuine absorption capacity. A household that is strong in one dimension and absent in another has a single-point failure in its resilience architecture.

Building the Emergency System: Failure Modes and Build Sequence

The Five Failure Modes — Emergency Systems

The Build Sequence: Why Order Matters

Emergency preparedness is commonly approached as a set of parallel tasks to be completed in any order. The HEPI research and FEMA resilience data suggest a different conclusion: preparedness dimensions are interdependent, and some layers enable others. Building them out of sequence produces a system with structural gaps.

Build financial preparedness first. The resilience buffer is the foundation layer. It is what converts every other category of disruption from a potential cascade event into a manageable incident. A household with six months of essential expenses in liquid savings and adequate insurance coverage has protected itself against the most consequential failure mode in every other preparedness dimension.

Build documentation and insurance second. Critical documents and insurance information need to be organized and accessible before a disruption makes them inaccessible. An insurance policy that cannot be located during a claim is functionally nonexistent. This layer requires two to three hours of focused work. It is one of the highest-leverage investments in the entire system.

Build plans and protocols third. A communication plan, established meeting points, and documented decision triggers require conversation and agreement with everyone in the household, and potentially with neighbors and extended family who are part of the support network. This is the social coordination layer, and it cannot be built alone or in a single sitting.

Build operational supplies and skills last. Once the first three layers are in place, the 72-hour supply kit and skills development address the operational gap for the period immediately following a disruption when professional services and supply chains may be temporarily unavailable. This layer matters. It is simply the least consequential of the four if the others are absent.

Running the System: The Annual Review and Off-Cycle Triggers

An emergency system built once and never reviewed degrades invisibly. Insurance policies fall out of alignment with current assets. Supply reserves pass expiration dates. Household composition changes like a new dependent, a move, a change in health status, and the plans do not update to reflect the new reality. The feedback loop for this domain is an annual review, scheduled on a fixed date, with a defined scope.

Annual Review Scope (allow 2–3 hours)

Insurance adequacy across all current policies. Resilience buffer status against current essential expense baseline. Document organization is necessary and you should consider are all critical documents current, accessible, and known to all relevant household members? Plan review: does the communication plan reflect the current household, and does every member know it? Supply check: what has expired or been used and not replaced?

Off-Cycle Review Triggers

Certain life changes make the annual cycle insufficient. Any of the following events should trigger an immediate partial review: a move to a new location (new hazard profile, new evacuation routes), a new household member (plans must include them), a significant income change (buffer target and insurance adequacy both shift), or a major asset acquisition (home purchase, vehicle, business). These events change the system inputs — the plan must change with them.

Run Your Emergency System Diagnostic

Open a blank document. Rate your current state honestly — not what you intend to build, but what exists right now — across each of the six HEPI preparedness dimensions. Use: IN PLACE / PARTIAL / ABSENT.

02 — PLANS & PROTOCOLS: Does your household have a documented communication plan and an established meeting point if normal contact fails? [ IN PLACE / PARTIAL / ABSENT ]

03 — SUPPLIES: Do you have at minimum 72 hours of water, food, and essential medications currently available in your home? [ IN PLACE / PARTIAL / ABSENT ]

04 — FINANCIAL BUFFER: Do you have 3+ months of essential expenses in liquid savings? (See Article #34 for the full resilience buffer framework.) [ IN PLACE / PARTIAL / ABSENT ]

05 — SOCIAL NETWORK: Do you have at least two neighbors or nearby contacts who know your household and could be a resource during a disruption? [ IN PLACE / PARTIAL / ABSENT ]

06 — DOCUMENTS & INSURANCE: Can you locate every insurance policy and piece of critical identification for your household in under 10 minutes right now? [ IN PLACE / PARTIAL / ABSENT ]

PRIORITY: Which dimension has the most cascade consequence if it remains ABSENT? Build that one first.

You now have an Emergency System Diagnostic. Every dimension marked ABSENT is a single-point failure in your resilience architecture. The build sequence is: financial layer first, documentation second, plans third, operational supplies and skills last. The support articles linked below build each layer in detail.